I usually prefer not to buy retail stocks; too volatile a sector for me. But Target $TGT, however, is one big-box retailer worth looking at to potentially add to the portfolio.

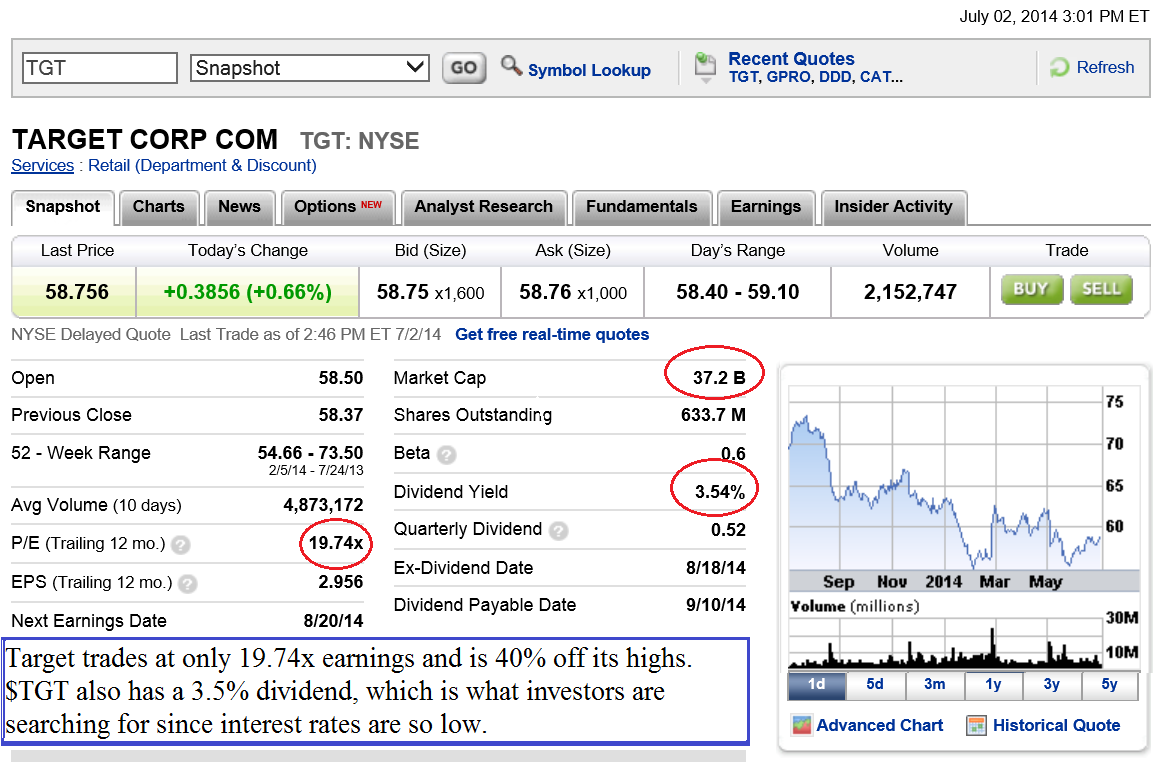

TGT’s valuation of 19x earnings is attractive. It is currently trading at 58.00 a share (nearly 40% off its highs) making valuation alone a compelling reason to buy Target.

$TGT also has a hefty 3.5% dividend and is considered a best of breed company on Wall Street. After all, it’s “red bullseye” logo makes it one of the most recognizable brands in the world.

19x earnings is a bit much though, you might say, compared to the S&P 500 which trades historically at around 18x earnings. However, a premium company like Target deserves a premium multiple, since one always pays up for quality in the stock market.

The S&P 500 had a killer run in June, so I am refraining from buying too many stocks at the moment. However, if I owned Target ($TGT) as the market started to fall, I would not be as worried about it as my other positions since the majority of its downside is already out.

$TGT is not the sexiest stock in the world, but it’s safe, and one worth mentioning seeing as how cheap it has gotten. Currently trading at $58.00 a share, I see Target ($TGT) as having a favorable risk/reward scenario of 3 points down ($55.00) and 10 points up ($70.00, old highs). The stop loss goes in at $53.90. Enjoy!